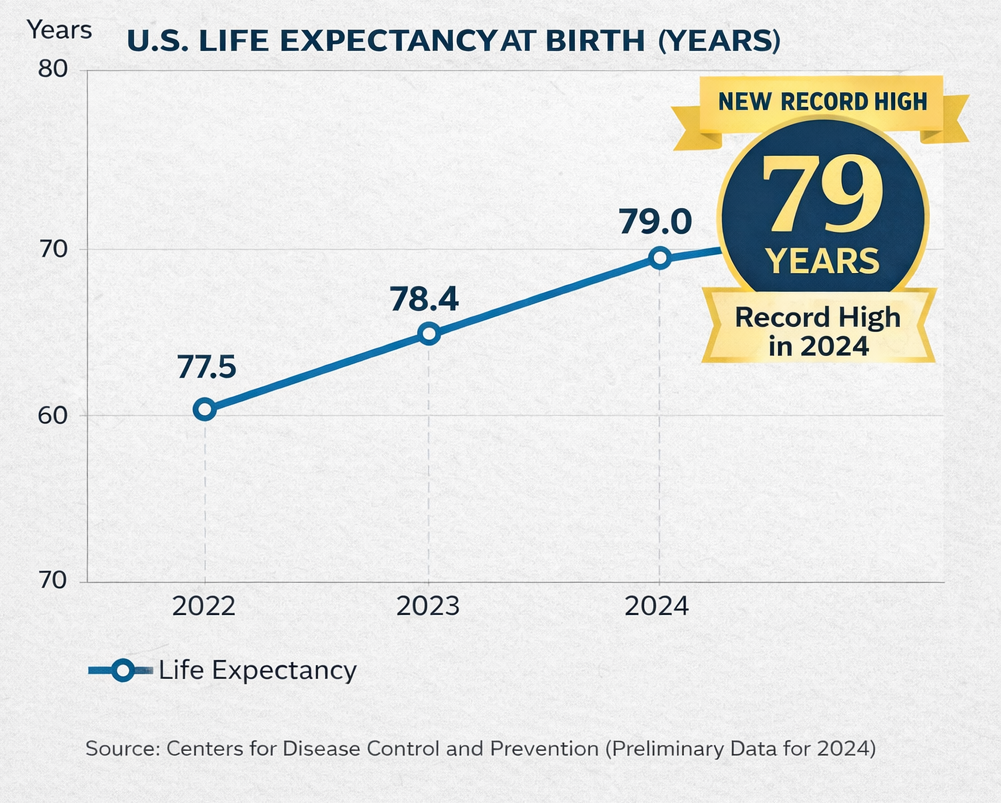

The Centers for Disease Control and Prevention recently shared some good news when it reported that life expectancy in the U.S. reached a record high of 79 years in 2024. That is an increase of 0.6 years from 2023, and 0.2 years higher than life expectancies in 2019.

The increase in life expectancy owes largely to improvements in death rates for chronic respiratory diseases, and lower death rates for both cancer and heart disease. Death rates fell for Americans in all age groups but improved the most for Americans aged 15 to 44.

While longer life expectancies at birth and lower death rates among all age groups are both to celebrated, there is another side of the coin to consider. Lower death rates and longer life expectancies threaten the retirement ecosystem in the United States that is already struggling.

Strains in the Retirement System

We are already aware of the challenges that many retirees and those who plan to retire soon face in the United States today. Private sector pension plans have all but disappeared from the retirement landscape over the past four decades, leaving employees to shoulder the burden of planning for their retirement. On the public employment front, huge unfunded pension liabilities continue to grow, threatening the comfortable retirement of public sector employees. In 2024, unfunded public pension liabilities across the U.S. were estimated to be almost $1.5 trillion.

And as we are reminded all too frequently in the news, Social Security is on life support. A major source of retirement for an overwhelming majority of Americans, Social Security is projected to be unable to pay promised benefits early in the 2030s. Meanwhile thousands of baby boomers retire daily further straining an unsustainable system. Our nation’s leaders have known about this problem for decades but have failed to act to fix the problem. Each additional day that Congress fails to address Social Security’s problems makes the cure to the problem more painful for taxpayers.

Finally, persistent inflation and healthcare costs that continue to outpace inflation threaten retirees’ livelihoods.

What additional impact will Americans living longer have on an already fragile retirement system?

What Can You Do to Better Prepare for Retirement?

It should be abundantly clear by now that you are going to be responsible for providing for your own comfortable retirement. Here are some things you can do to ensure your Golden Years aren’t tarnished.

Save more and save better.

Saving an adequate amount for retirement is only one-half of the equation. We also need to find better ways to save. Workers who have access to Health Savings Accounts (HSAs) should be funding these accounts to the maximum amount allowed annually. Beyond that, careful consideration is required to determine whether your retirement contributions should be allocated to pre-tax, Roth or non-qualified accounts.

Uncertainty about future income tax rates complicates the analysis.

Rethink what retirement looks like.

We don’t live like our parents or grandparents did at our age, why should we retire the same way? The days of retiring at age 62 with a gold watch and a pension are gone forever. Transitioning to retirement may be a phased approach for many Americans rather than an abrupt one-time event.

Hybrid and flexible work arrangements are becoming more common, as are later-in-life career changes to vocations that provide more fulfillment and flexibility, and may lead to Americans working in some capacity into their seventies or even eighties.

Invest prudently and spend moderately.

Longer life expectancies may necessitate longer retirement phases for many Americans, which ultimately means their retirement nest eggs must also last longer. This creates a very complicated equation of balancing the need for reliable investment returns that protect retirees from inflation and an uncertain time horizon for which their retirement savings must last, while also accounting for unexpected costs and expenditures at various times in retirement. A very tricky endeavor indeed!

What we are ultimately talking about here is longevity risk: the risk of outliving your retirement assets. The good news is that you don’t have to navigate this challenge alone.

The team at Bollin Wealth Management has decades of experience helping Americans retire and maintain a comfortable lifestyle in retirement. Give us a call today to ensure a longer life expectancy doesn’t put your comfortable retirement at risk.

Sources: The Wall Street Journal, National Center for Health Statistics, Centers for Disease Control and Prevention